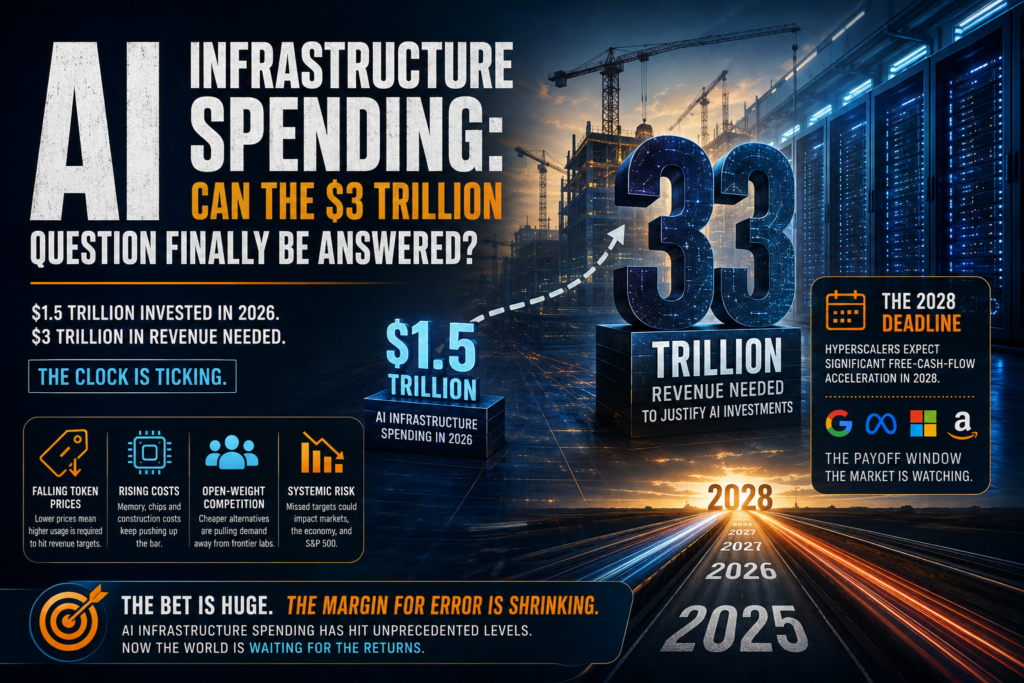

AI infrastructure spending has crossed a threshold that even its biggest champions are starting to question out loud. The short answer: the AI industry now needs to generate roughly $3 trillion in cumulative revenue to justify the capital poured into chips and data centers through 2026 — and right now, the gap between what’s been spent and what’s been earned is still enormous. Whether that gap closes fast enough may decide the next few years of the broader economy.

This isn’t a new anxiety. It’s an old one that keeps getting bigger.

What Is the $3 Trillion AI Question?

The “$3 trillion question” traces back to a calculation popularized by Sequoia partner David Cahn. In 2023, <cite index=”1-2,1-3″>Cahn responded to Nvidia’s reported annual GPU revenue of $50 billion by calculating that the AI industry would need $200 billion in revenue to pay back the upfront infrastructure investment, once data center operating costs and operator margins were factored in.</cite> At the time, that framing was meant less as a doomsday prediction and more as a challenge — <cite index=”1-4″>Cahn used it to push entrepreneurs to build AI products and services that could actually generate revenue from all the infrastructure being built.</cite>

Three years later, the numbers have grown far past that original estimate. <cite index=”1-5″>Cahn’s updated calculation puts 2026 AI infrastructure spending at $1.5 trillion.</cite> <cite index=”1-6″>Taken together with prior years of buildout, he estimates the AI industry needs to earn $3 trillion in revenue to justify the total chip and data center spending to date.</cite>

Why This Number Keeps Rising

The $3 trillion figure isn’t fixed — and it’s more likely to climb than shrink. <cite index=”1-7″>Cahn notes that this is probably an underestimate, since rising memory costs and growing reliance on specialized inference chips will likely push the required revenue even higher.</cite> <cite index=”1-7″>He points specifically to a sharp recent increase in the required revenue per gigawatt of capital expenditure, driven by these bottleneck dynamics and rising construction costs.</cite>

That distinction matters for anyone tracking AI infrastructure spending as an investment thesis rather than just a headline number. It’s not simply “how much have we spent” — it’s “how much more will we need to spend just to keep the current buildout running,” which pushes the breakeven point further out.

How Much Are Hyperscalers Actually Spending?

From $50 Billion to $1.5 Trillion in Three Years

The scale-up has been staggering. What began as a single-year GPU revenue figure for one company has become an annual industry-wide infrastructure spending number thirty times larger. This is the core tension driving every AI ROI debate happening in boardrooms and on earnings calls right now: infrastructure spending has compounded far faster than most companies’ ability to monetize it directly.

Revenue Is Growing Too — Just Not Fast Enough

The revenue side of the ledger has moved as well, though nowhere near the pace of the spending side. <cite index=”1-8″>Anthropic is reported to have reached $60 billion in annualized revenue, while OpenAI reportedly earned $13 billion in 2025.</cite> <cite index=”1-8″>By November 2025, OpenAI said it had reached $20 billion in annualized revenue, alongside roughly $1.4 trillion in data center commitments.</cite>

Put simply: even the fastest-growing AI companies in history are earning tens of billions of dollars a year against trillions in committed infrastructure spending. That mismatch is the entire reason the $3 trillion question exists.

AI Infrastructure Spending vs. Revenue: The Numbers Side by Side

| Metric | Figure | Source Context |

|---|---|---|

| 2026 estimated AI infrastructure spending | ~$1.5 trillion | David Cahn / Sequoia analysis |

| Total revenue needed to justify cumulative spend | ~$3 trillion | David Cahn / Sequoia analysis |

| Anthropic annualized revenue | ~$60 billion | Reported industry estimate |

| OpenAI 2025 revenue | ~$13 billion | Reported financial data |

| OpenAI annualized revenue (Nov. 2025) | ~$20 billion | Sam Altman, public statement |

| OpenAI data center commitments | ~$1.4 trillion | Sam Altman, public statement |

| Hyperscaler free-cash-flow inflection point (projected) | 2028 | Torsten Slok / Apollo |

The table makes the imbalance easy to see: even combining Anthropic’s and OpenAI’s revenue doesn’t come close to matching a single year of industry-wide AI infrastructure spending, let alone the cumulative total.

Why Falling Token Prices Complicate the ROI Math

This is where the AI infrastructure spending story gets more uncomfortable. It’s not just that revenue is behind spending — it’s that the price of the underlying product, AI tokens, is actively falling.

Is AI infrastructure spending being undercut by cheaper models? Yes, and the trend is accelerating. <cite index=”1-9,1-10″>Apollo chief economist Torsten Slok has pointed to a growing risk: organizations increasingly adopting cheaper open-weight models, often built in China, instead of frontier lab offerings, alongside falling token prices industry-wide.</cite>

Efficiency gains are compounding the problem for anyone counting on rising per-token revenue to fund AI infrastructure spending commitments. <cite index=”1-11″>OpenAI CEO Sam Altman has said the company’s newest model is 54% more token-efficient on coding tasks than its predecessor.</cite> That’s unambiguously good news for developers and businesses managing AI agent costs. It’s a much harder problem for companies that built their entire capital plan around users consuming ever-more tokens at stable or rising prices.

The Efficiency Paradox

- For users: Lower token prices and higher efficiency mean cheaper AI agents and lower operating costs — a clear win.

- For infrastructure operators: The same efficiency gains mean each GPU-hour generates less revenue unless overall usage volume rises to compensate.

- For the $3 trillion target: Falling prices raise the bar even further, since more total usage is now required to hit the same revenue goal.

- For open-weight competition: Cheaper alternative models pull demand away from the frontier labs whose revenue is supposed to close the AI ROI gap in the first place.

This is the paradox sitting at the center of the current AI infrastructure spending debate: the technology is becoming more efficient and more useful, but that same efficiency makes the original financial bet harder to win.

The 2028 Free-Cash-Flow Bet

Wall Street’s patience with AI infrastructure spending isn’t unlimited, but it has a specific expiration date built into current forecasts. <cite index=”1-9″>Slok has observed that Google, Meta, Microsoft, and Amazon are all projecting significant free-cash-flow accelerations in 2028 — the point at which they expect to see the payback from their infrastructure investment.</cite>

That single year — 2028 — has effectively become the deadline the market has set for AI infrastructure spending to prove itself. Every quarterly earnings call between now and then will be read partly through that lens: are the hyperscalers on pace, ahead, or falling behind their own projections?

What Happens If the 2028 Targets Are Missed?

This is where the stakes stop being an industry story and start being a macroeconomic one. <cite index=”1-12″>Slok has warned that because so much of the market is concentrated in so few companies, a slower-than-expected payoff on AI infrastructure spending wouldn’t just be a sector-specific problem — it could risk tipping the broader economy into recession and pulling the S&P 500 into a correction.</cite>

That’s a notable escalation from where this conversation started in 2023. Back then, the $200 billion question was framed as a challenge to founders: build something worth the infrastructure. Today’s $3 trillion question is framed as a systemic risk: if the payoff doesn’t arrive on schedule, the consequences may not stay contained to AI companies or even to the tech sector.

How Does This AI Infrastructure Spending Cycle Compare to Past Tech Buildouts?

Comparisons to the dot-com era and the telecom fiber buildout of the late 1990s are common in this debate, and they’re useful — up to a point.

- Scale: The dot-com infrastructure buildout was measured in the tens of billions; current AI infrastructure spending is measured in the trillions, an order-of-magnitude difference.

- Concentration: Unlike the fragmented dot-com landscape, today’s AI infrastructure spending is concentrated among a small handful of hyperscalers and frontier labs, which is precisely why Slok flags systemic risk rather than sector risk.

- Revenue visibility: Dot-com infrastructure often preceded any working business model. Today’s AI labs already have real, fast-growing revenue — it’s simply not yet proportional to the capital deployed.

- Efficiency trajectory: Telecom fiber capacity took years to be “used up.” AI token efficiency is improving so quickly that the useful lifespan of any given compute investment is harder to predict.

The comparison isn’t a perfect analogy, but it explains why economists like Slok are watching this cycle so closely: the combination of massive scale and high concentration means the downside risk, if the ROI thesis fails, is unusually correlated across the market.

Frequently Asked Questions About AI Infrastructure Spending

What is the “$3 trillion question” in AI? It refers to Sequoia partner David Cahn’s estimate that the AI industry needs roughly $3 trillion in cumulative revenue to justify the total capital spent on chips and data centers, based on his running analysis of hyperscaler CapEx since 2023.

How much is being spent on AI infrastructure in 2026? Cahn’s latest estimate puts 2026 AI infrastructure spending at approximately $1.5 trillion, up dramatically from the $50 billion in annual GPU revenue that first prompted his analysis in 2023.

Are AI companies making enough money to justify the spending? Not yet, based on current figures. Anthropic’s reported $60 billion in annualized revenue and OpenAI’s reported $13–20 billion range are both far below the multi-trillion-dollar spending levels they’re meant to eventually offset.

Why are falling token prices a risk for AI infrastructure spending? Because much of the financial case for AI infrastructure spending depends on rising revenue per unit of compute. As models become more efficient and cheaper open-weight alternatives gain adoption, revenue per token can fall even as usage grows — making the breakeven math harder to hit.

When will we know if AI infrastructure spending has paid off? Major hyperscalers — Google, Meta, Microsoft, and Amazon — are projecting sharp free-cash-flow improvements starting in 2028, which analysts are treating as the informal deadline for the current AI ROI thesis to prove out.

What happens if AI infrastructure spending doesn’t pay off by 2028? According to Apollo’s Torsten Slok, given how concentrated the market is in a small number of AI-exposed companies, a disappointing payoff could extend beyond the tech sector — potentially contributing to broader economic recession risk and a correction in the S&P 500.

The Bottom Line on AI Infrastructure Spending

The AI ROI debate hasn’t gone away — it’s simply gotten bigger, along with every number attached to it. AI infrastructure spending has scaled thirty-fold in three years, revenue has grown but not proportionally, token prices are falling even as efficiency improves, and the market has effectively set a 2028 deadline for the math to work out. None of this means the bet will fail. It does mean the margin for error is shrinking as the dollar figures grow, and that anyone building on top of this infrastructure — from founders to investors to enterprise buyers — has real reason to watch how this plays out over the next two years.