Space data centers are no longer science fiction — they are the infrastructure battleground of the 2030s. As artificial intelligence devours compute power faster than Earth’s power grids can keep up, a new class of startups is racing to put data centers in orbit. The biggest obstacle? There aren’t enough rockets to get them there.

That is the exact problem Cowboy Space Corporation raised $275 million in May 2026 to solve — by building its own rockets.

What Are Space Data Centers?

Definition: A space data center is an orbital computing facility — a satellite equipped with processors, memory, and power generation systems — designed to run AI workloads, edge computing tasks, or data processing operations from low Earth orbit (LEO).

Unlike terrestrial data centers constrained by land costs, cooling requirements, power availability, and regulatory zoning, space data centers draw on abundant solar energy in orbit and radiate excess heat into the thermal vacuum of space. In theory, they can scale compute capacity without the geographic and environmental bottlenecks that are already slowing AI infrastructure expansion on the ground.

The concept has moved from speculative to investable very quickly. Multiple well-funded ventures — including Google’s Project Suncatcher, Starcloud, and now Cowboy Space Corporation — are actively developing orbital computing platforms, each with different timelines and technical approaches.

The Rocket Bottleneck: Why Getting to Orbit Is the Hard Part

Space data centers face an upstream constraint that has nothing to do with software, chip design, or power management: launch capacity is severely limited, and it may stay that way for years.

The economics of orbital AI are brutal partly because of this dependency. Even when a company designs a viable satellite data center, it cannot scale without reliable, affordable, and frequent access to orbit. And right now, that access simply does not exist at the scale the industry needs.

Why SpaceX and Blue Origin Aren’t the Answer (Yet)

The two most powerful rockets under development — SpaceX’s Starship and Blue Origin’s New Glenn — are widely seen as potential solutions to the launch capacity problem. Both vehicles are designed to carry very large payloads to orbit at reduced per-kilogram costs. But neither is commercially available to third parties on a meaningful timeline.

SpaceX’s Starship, which was preparing for its twelfth test flight as of May 2026, is expected to be consumed by the company’s own Starlink satellite megaconstellation once it becomes operational. Blue Origin’s New Glenn failed to deliver a satellite during its third launch in April 2026, underscoring how far it remains from reliable commercial service.

Other contenders — Rocket Lab, Stoke Space, Firefly Aerospace, Relativity Space — are still working their way through development cycles. Only a handful of Western launch providers are consistently putting commercial payloads into orbit today.

The Launch Capacity Gap in Numbers

The gap becomes clearer when examined against what space data center companies actually need:

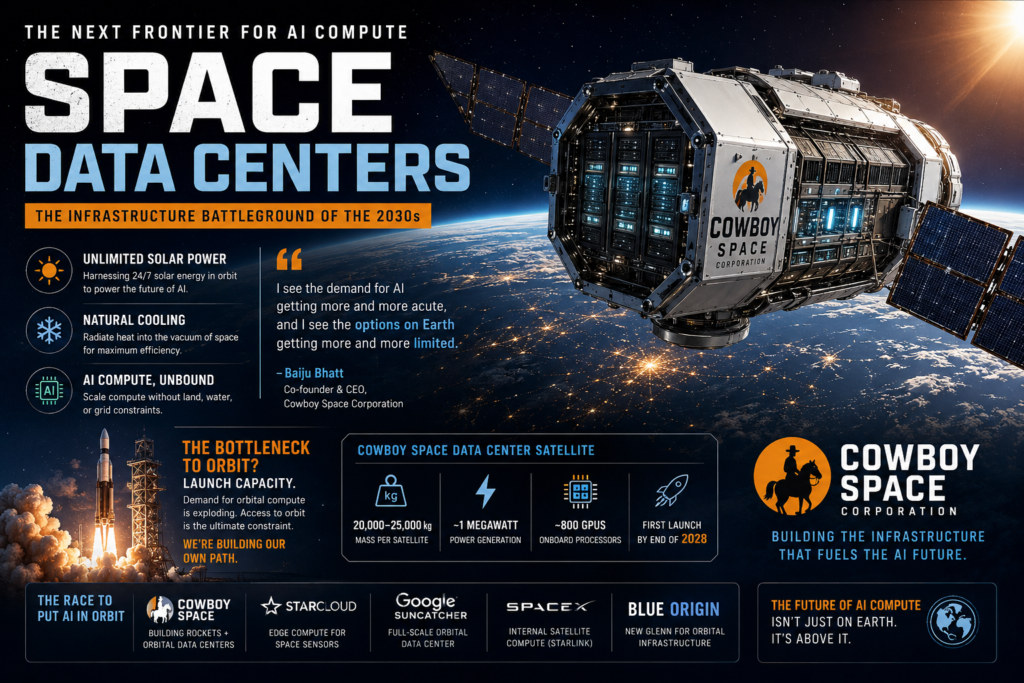

- Cowboy Space’s target satellite mass: 20,000–25,000 kg per unit

- Power generation per satellite: ~1 megawatt (MW)

- GPUs per satellite: ~800 onboard processors

- Comparable rocket class required: Slightly more powerful than a Falcon 9, smaller than Starship

At that scale, a single launch delivers meaningful compute — but scaling to hundreds of satellites requires hundreds of launches. With commercial launch slots scarce and expensive, and first-party rocket providers prioritizing internal payloads, space data center companies are functionally locked out of the market unless they control their own access to orbit.

Cowboy Space Corporation: Building Its Own Path to Orbit

What is Cowboy Space Corporation? Cowboy Space Corporation (formerly Aetherflux) is a U.S. space infrastructure startup founded in 2024 by Baiju Bhatt — co-founder of the stock trading platform Robinhood — with the mission of building and operating orbital data centers powered by solar energy collected in space.

The company’s pivot from solar energy beaming to orbital computing to rocket development is a textbook case of a startup following the logic of its constraints all the way to their source.

From Solar Energy Startup to Space Infrastructure Company

Bhatt originally launched the company as Aetherflux in 2024, focused on a genuinely ambitious idea: collect abundant solar energy in orbit and beam it down to Earth as a clean power source. As the company explored the practical realities of that concept, space-based data centers emerged as a more immediate and commercially viable use for the electricity generated in orbit — why beam it down when you can use it right there?

But then came the harder question: how do you get enough satellites into orbit to make the business viable? Bhatt engaged multiple launch providers looking for a path where Cowboy Space would only need to build the satellites. The answer was that sufficient launch capacity simply did not exist — not at competitive unit economics, and not on a timeline that matched the AI infrastructure opportunity.

The logical conclusion? Build the rocket.

The $275 Million Bet on Vertical Integration

In May 2026, Cowboy Space announced the close of a $275 million Series B round at a post-money valuation of $2 billion. Index Ventures led the round, with participation from Breakthrough Energy Ventures, Construct Capital, IVP, and SAIC.

The capital is earmarked to fund simultaneous development across three domains:

- Rocket development — building a proprietary launch vehicle targeting a first launch before the end of 2028

- Satellite development — designing the orbital data center hardware that will serve as the rocket’s payload and final stage

- Engine development — building a proprietary rocket engine, the most complex and expensive component of any launch system

To staff those programs, the company has hired talent directly from the industry’s leading players, including former Blue Origin propulsion engineer Warren Lamont and former SpaceX launch director Tyler Grinne.

How the Satellite-as-Rocket-Stage Design Works

One of the most technically distinctive aspects of Cowboy Space’s approach is the integration of the data center into the rocket’s second stage. Rather than designing a satellite as a separate payload delivered by a generic upper stage, Cowboy Space builds its compute hardware directly into the stage that achieves orbit.

This concept has a historical precedent: Explorer 1, the first U.S. satellite launched in 1958, was essentially the final stage of a Juno I rocket filled with scientific instruments and a radio transmitter. Cowboy Space is applying that same logic at a vastly different scale.

The advantages of this approach include:

- Simplified design process — the rocket is purpose-built for a single payload type, reducing the engineering surface area

- Reduced mass overhead — no separate fairing or payload adapter structure is required

- Tighter integration — thermal management and power routing can be co-designed from the start

The company’s target spec — 20,000–25,000 kg satellites, 1 MW of power, ~800 GPUs — positions each unit as a meaningful compute node in its own right, even before any constellation-level aggregation.

Who Else Is Racing to Put AI in Orbit?

Cowboy Space is not operating in isolation. The orbital computing market is attracting significant capital and talent, with players taking meaningfully different approaches to the same fundamental challenge.

| Company | Approach | Timeline | Key Constraint |

|---|---|---|---|

| Cowboy Space Corporation | Build own rockets + orbital data centers | First launch by end of 2028 | Rocket development risk |

| Starcloud | Edge compute for space sensors; raised $170M Series A (March 2026) | Near-term commercial ops | Limited to smaller payloads |

| Google Suncatcher | Full-scale orbital data center backed by Alphabet | Mid-2030s target | Dependent on Starship availability |

| SpaceX (Starlink) | Internal satellite compute for own constellation | Ongoing | Not commercially available |

| Blue Origin | New Glenn rocket for orbital infrastructure | TBD post-development | Still in development phase |

The competitive landscape divides roughly into two camps: those waiting for large rockets to become commercially available (Google Suncatcher, and most others), and those trying to create their own launch capacity (Cowboy Space). The former group is targeting the mid-2030s; the latter is targeting late 2028.

Why Space Data Centers Could Reshape AI Infrastructure

The Energy Advantage

The most compelling structural argument for space data centers is energy. On Earth, AI compute infrastructure is running headlong into power constraints: data centers require vast amounts of electricity, generate enormous heat, and are increasingly competing with residential and industrial consumers for grid capacity. In many regions, permitting a new large-scale data center has become as difficult as siting a power plant.

In orbit, solar panels receive sunlight 24 hours a day with no atmospheric attenuation, producing roughly 1.4 kW per square meter of panel area — significantly more than terrestrial solar. Heat rejection in the vacuum of space is highly efficient via radiation. There are no zoning boards, no water cooling requirements, no air quality permits.

Space data centers, if built at scale, could deliver compute capacity that is structurally decoupled from the land, water, and grid constraints that are increasingly binding terrestrial AI infrastructure.

The Latency and Scaling Argument

Low Earth orbit satellites operate at altitudes of roughly 300–2,000 km. At those distances, the round-trip latency for a signal traveling between the satellite and Earth is in the range of 2–20 milliseconds — comparable to a cross-continental fiber connection and far better than geostationary satellites.

For AI workloads that do not require sub-millisecond response times — model inference for batch tasks, training jobs, large-scale data analysis — orbital compute could serve as a genuine alternative to ground-based infrastructure. Baiju Bhatt framed the opportunity directly: “I see the demand for AI getting more and more acute, and I see the options on Earth getting more and more limited.”

The Risks and Realities: What Could Go Wrong

Honest assessment of space data centers demands engagement with the substantial risks involved. The sector is compelling in theory; execution is another matter entirely.

Technical risks specific to space data centers include:

- Radiation effects on hardware: Processors operating in orbit are exposed to charged particle radiation that degrades semiconductor performance over time and causes bit-flip errors. Radiation-hardened hardware is expensive and often less powerful than commercial equivalents.

- Thermal management at scale: Radiating 1 MW of waste heat from a satellite is a serious engineering challenge. Conventional satellite thermal systems are designed for far lower power densities.

- On-orbit servicing: Unlike a terrestrial data center where a technician can swap a failed GPU, orbital hardware is effectively unreachable. Mean time between failures must be extraordinarily low.

- Debris risk: Low Earth orbit is increasingly congested. A collision with debris — even a paint chip at orbital velocities — can be catastrophic for a large, high-value satellite.

Business and execution risks include:

- Rocket development is extraordinarily hard. SpaceX, Blue Origin, and ULA have collectively spent decades and tens of billions of dollars developing reliable orbital launch vehicles. Cowboy Space is attempting this in a compressed timeline with a fraction of that capital.

- The competition is better funded. SpaceX and Blue Origin are the most advanced and well-resourced players in this market. Cowboy Space will be in direct competition with them for launch manifest slots, talent, and eventually customers.

- The unit economics are unproven. No company has yet demonstrated that orbital AI compute can compete with terrestrial alternatives on cost-per-FLOP at commercial scale. The theoretical advantages must translate to viable pricing.

What This Means for the Future of AI Compute

Space data centers represent a genuine inflection point in how the industry thinks about AI infrastructure — not because they will replace terrestrial data centers, but because they may relieve the most binding constraints on scaling them.

The AI compute shortage is structural. Demand for inference and training capacity is growing faster than the power grid, construction schedules, and semiconductor supply chains can accommodate. Space-based infrastructure offers a path to additional capacity that is not bottlenecked by the same factors as ground-based alternatives.

Cowboy Space’s bet is that vertical integration — owning the rocket, the engine, and the satellite — is the only defensible path to building orbital data centers at commercial scale on a timeline that matters. If the bet pays off, the company would be among the first to operate space data centers as a commercial service, ahead of competitors who are waiting for Starship.

If it fails, it will at minimum validate the core thesis and clarify the technical barriers for whoever comes next.

Either way, the race to build space data centers has moved from the domain of conceptual papers to funded startups with hired engineers, signed leases, and a first launch target less than three years away. The frontier is no longer metaphorical.

Frequently Asked Questions

What are space data centers, and why do they matter for AI? Space data centers are computing facilities deployed as satellites in low Earth orbit. They matter for AI because they can access abundant solar power and efficient thermal radiation in space, potentially bypassing the land, water, and grid constraints that are slowing expansion of terrestrial AI infrastructure.

Why is Cowboy Space Corporation building its own rocket? Cowboy Space found that commercial launch capacity — from SpaceX, Blue Origin, and others — is insufficient to scale an orbital data center business at competitive unit economics. After conversations with multiple launch providers, founder Baiju Bhatt concluded that vertical integration (owning the rocket) was the only viable path forward.

When will space data centers be commercially operational? Timelines vary by company. Cowboy Space is targeting a first rocket launch before the end of 2028. Google’s Suncatcher project is targeting the mid-2030s. Starcloud, which focuses on smaller edge compute satellites, is the closest to near-term commercial operations as of 2026.

How many GPUs can a space data center satellite carry? Cowboy Space’s target specification is approximately 800 GPUs per satellite, with each satellite generating roughly 1 MW of power and weighing 20,000–25,000 kg.

Conclusion

The rise of space data centers signals a major turning point in the future of artificial intelligence infrastructure. As AI workloads continue growing at an unprecedented pace, traditional data centers on Earth are facing increasingly difficult limitations related to power consumption, cooling efficiency, land availability, environmental regulations, and grid capacity. These challenges are no longer theoretical—they are already slowing the expansion of AI infrastructure worldwide. This is exactly why space data centers are becoming one of the most important long-term solutions for scalable AI compute.

Unlike terrestrial facilities, space data centers offer access to uninterrupted solar energy, natural thermal radiation, and virtually unlimited expansion opportunities in orbit. This creates a compelling foundation for next-generation AI infrastructure that is not constrained by the same bottlenecks affecting Earth-based operations. The ability of space data centers to generate power in orbit while supporting large-scale compute workloads could fundamentally reshape how AI companies think about infrastructure deployment over the next decade.

Cowboy Space Corporation’s recent funding round highlights growing investor confidence in the commercial viability of space data centers. By vertically integrating rocket development, satellite engineering, and orbital compute systems, the company is attempting to solve the most critical problem in the sector: launch access. Without affordable and frequent launches, even the most advanced space data centers cannot scale. This makes rocket ownership a strategic advantage rather than just an operational choice.

However, the path forward is still filled with technical and economic challenges. Radiation exposure, thermal management, hardware failures, orbital debris, and launch reliability remain serious risks. The success of space data centers will depend on whether companies can overcome these engineering hurdles while proving sustainable unit economics against terrestrial alternatives.

Even with these uncertainties, one fact is becoming increasingly clear: AI’s compute demand is outpacing Earth’s infrastructure capacity. As a result, space data centers are no longer a distant science fiction concept—they are an emerging infrastructure category attracting real capital, talent, and commercial ambition. Over the next decade, the companies that successfully build scalable space data centers could define the next era of AI infrastructure and create an entirely new layer of global computing capability beyond Earth. The future of compute may not be built only on land—it may be built in orbit.