TCS AI revenue crossed $2.6 billion in annualized run rate for Q1 FY27, up from roughly $2.3 billion a quarter earlier. But the growth is lumpy, project-driven, and far from the predictable, recurring income stream that investors associate with a true “annuity” business — and that gap is now the central question hanging over India’s largest IT services company.

TCS AI Revenue in Q1 FY27: The Numbers at a Glance

Run-Rate Snapshot

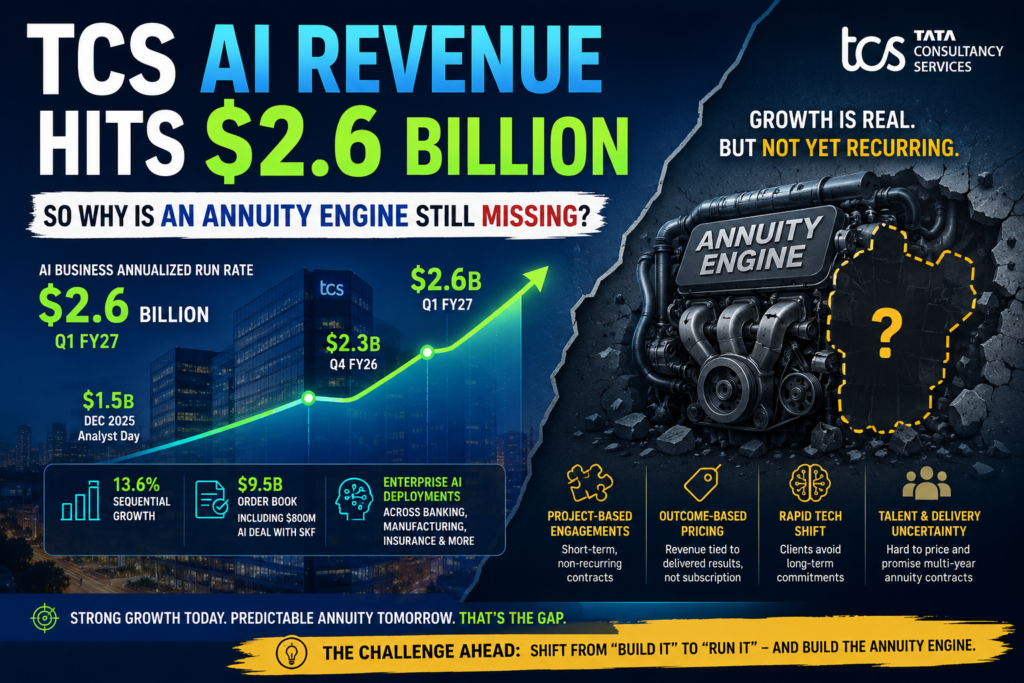

Tata Consultancy Services closed the June 2026 quarter with its AI business at a $2.6 billion annualized revenue run rate, a 13.6% sequential jump. CEO K Krithivasan framed this scale-up alongside a strong $9.5 billion order book, which included a marquee $800 million AI-led transformation deal with industrial manufacturer SKF. On the surface, this looks like a genuine AI growth story: enterprise clients are moving beyond pilot projects into large-scale, production-grade AI deployments spanning banking, manufacturing, insurance, and consumer businesses.

Timeline: How the AI Business Has Scaled

TCS didn’t arrive at $2.6 billion overnight. In December 2025, the company disclosed $1.5 billion in annualized AI revenue at its Analyst Day, describing AI as a “civilizational change” in how enterprises operate. By Q4 FY26, that figure had climbed to roughly $2.3 billion. The jump to $2.6 billion in Q1 FY27 continues the upward trend, but the pace of quarter-over-quarter dollar additions has clearly decelerated even as the percentage growth rate stays in double digits — a pattern worth watching closely over the next two to three quarters.

Incremental Growth Is Slowing, Not Accelerating

Here’s the catch. While the percentage growth in TCS AI revenue looks healthy, the absolute incremental addition tells a different story. Quarterly AI revenue added roughly $75 million in Q1 FY27 — down sharply from about $125 million in the prior quarter. That deceleration is the clearest evidence yet that the underlying business is not compounding on a stable base; it is being added in discrete, project-sized chunks that can just as easily shrink as they can grow.

To put that in perspective: a company with a true annuity engine would expect incremental quarterly additions to stay roughly flat or rise steadily as the base grows, because renewed contracts keep contributing on top of new wins. A near-40% drop in incremental dollars added — from $125 million to $75 million — is the kind of swing you’d expect from a project pipeline, where one or two large deals closing (or slipping into the next quarter) can move the needle disproportionately.

Executives themselves acknowledged this. Management attributed the choppiness to the fundamentally project-based nature of AI engagements — short-duration, non-recurring contracts rather than long-term managed-services relationships. That single admission is the crux of the “annuity engine” problem.

What Is an “Annuity Engine,” and Why Doesn’t TCS Have One in AI Yet?

Definition + Expansion: Annuity Revenue vs. Project Revenue

In IT services parlance, annuity revenue refers to income from long-term, recurring contracts — typically managed services, outsourcing, or infrastructure agreements that run for three, five, or even ten years with predictable renewal cycles. Project revenue, by contrast, comes from time-bound engagements: a specific AI pilot, a modernization sprint, or a one-off transformation initiative that ends once the deliverable is complete.

Traditional IT services — application maintenance, infrastructure management, BPO — built the annuity engine that has powered TCS’s balance sheet for two decades. It’s the reason IT services stocks trade at premium valuations: revenue visibility. This revenue, however, currently behaves more like the old project-based consulting model than the annuity model that investors are used to. A single large deal closing or slipping can swing quarterly AI numbers by tens of millions of dollars, which is exactly what happened between Q4 FY26 and Q1 FY27.

Why AI Deals Stay Project-Based

There are structural reasons AI engagements resist annuitization, at least for now:

- Maturity curve: Most enterprise AI initiatives are still in build-and-prove phases rather than steady-state operations, so contracts are scoped around outcomes, not ongoing service levels.

- Pricing experimentation: Clients are increasingly pushing for output-based and outcome-based pricing instead of the time-and-materials or fixed-annuity models common in legacy IT outsourcing, which by design ties revenue to delivered results rather than a subscription.

- Rapid technology shifts: Underlying AI models, agent frameworks, and tooling change quickly enough that clients hesitate to lock into multi-year commitments the way they would for stable infrastructure management.

- Talent and delivery uncertainty: Autonomous and agentic AI delivery models are still being defined internally at TCS itself, making it harder to price a five-year annuity contract with confidence.

Until AI work shifts from “build it” to “run it,” TCS AI revenue will keep behaving like a project pipeline rather than an annuity book.

Q: How is this different from how TCS built its traditional IT annuity business? A: Traditional infrastructure and application management contracts were sold as multi-year service-level agreements from day one, because the underlying technology — servers, networks, enterprise applications — was already mature and stable. AI, by contrast, is being sold while the technology itself is still evolving quarter to quarter, which naturally pushes contracts toward shorter, outcome-defined scopes rather than open-ended, multi-year commitments.

TCS Q1 FY27 Financial Performance Beyond AI

The AI story sits inside a broader Q1 FY27 result that was solid but not spectacular. TCS reported consolidated revenue of roughly ₹72,275 crore (about $7.58 billion), up 13.9% year-on-year and 2.2% sequentially, aided by strength in banking clients and favorable currency movements. Consolidated net profit came in at approximately ₹13,349 crore (about $1.40 billion), up around 5% year-on-year but down roughly 2.7% sequentially. Operating margin held at 24%, though it slipped by about 130 basis points quarter-on-quarter due to annual salary increments.

| Metric | Q1 FY27 | Change (QoQ) | Change (YoY) |

|---|---|---|---|

| Revenue | ~$7.58 billion (₹72,275 crore) | +2.2% | +13.9% |

| Net Profit | ~$1.40 billion (₹13,349 crore) | -2.7% | +5% |

| Operating Margin | 24% | -130 bps | — |

| AI Revenue (annualized run rate) | $2.6 billion | +13.6% | — |

| Total Contract Value (TCV) | $9.5 billion | — | — |

| Headcount | 593,798 | +~9,300 employees | — |

| Attrition (LTM) | 13.6% | — | — |

TCS also added around 9,300 employees in the quarter — its strongest quarterly hiring pace in more than three years — even as the industry continues to debate whether AI-driven automation will shrink IT services headcount. Client-tier data was mixed: the number of clients contributing over $10 million annually rose to 504 and $1 million-plus clients climbed to 1,401, but the $20 million-plus client cohort actually declined by four accounts to 307, suggesting some softness at the very top of the client relationship pyramid even as the broader base expanded.

That combination — broad-based client growth paired with softness among the very largest accounts — mirrors the AI revenue pattern almost exactly. TCS is winning more relationships and more deals in aggregate, but the biggest, most valuable engagements are the ones showing the most volatility quarter to quarter. Total contract value for the quarter reached $9.5 billion, with North America contributing $4.7 billion, BFSI (banking, financial services, and insurance) $2.5 billion, and consumer business $1.4 billion — evidence that deal-making momentum remains broad, even if AI-specific revenue recognition is choppier than the headline TCV suggests.

The HyperVault Bet: TCS’s Real Annuity Play

Data Centres as Recurring Revenue

If TCS AI revenue from services remains project-based, the company’s clearest attempt at building an actual annuity engine sits elsewhere: its data-centre subsidiary, HyperVault AI Data Center Limited. TCS has explicitly said this initiative is designed to secure long-term committed and annuity revenues from hyperscalers and AI companies leasing compute capacity, rather than one-off project fees. Unlike client-specific AI transformation deals, data-centre leasing agreements are structured more like real-estate or utility contracts — long tenors, contracted capacity, and predictable renewal economics.

TCS has already secured a $1 billion investment from global asset manager TPG to accelerate HyperVault’s build-out, and reports suggest OpenAI is in advanced discussions to become an anchor tenant leasing at least 500 megawatts of capacity. If that deal materializes, it would represent exactly the kind of multi-year, capacity-backed annuity contract that TCS’s core AI services business currently lacks.

How It Differs from AI Services Contracts

The distinction matters for anyone trying to understand where TCS AI revenue is headed:

| Dimension | AI Services (Current) | HyperVault Data Centres (Emerging) |

|---|---|---|

| Contract length | Months to ~1 year per engagement | Multi-year, capacity-based leases |

| Revenue pattern | Lumpy, project-driven | Recurring, annuity-style |

| Pricing model | Increasingly outcome/output-based | Fixed capacity + committed revenue |

| Client relationship | Enterprise transformation buyers | Hyperscalers, AI infrastructure tenants |

| Predictability | Low quarter-to-quarter | High once contracted |

In short, TCS is pursuing two very different monetization paths under the same “AI business” umbrella — one project-heavy and client-facing, one infrastructure-heavy and annuity-oriented. The second is still in its early innings.

TCS AI Revenue in Context: How the Broader IT Sector Is Positioned

TCS isn’t alone in navigating this transition. Rival Infosys closed FY26 with revenue just above $20 billion and reported large deal wins of $14.9 billion for the year, alongside its own AI-first consulting push built around a proprietary AI framework and guidance of 1.5–3.5% constant-currency revenue growth for FY27 — a range that itself signals how cautiously the sector is projecting near-term growth despite AI enthusiasm. Across the Indian IT sector, the pattern is similar: firms are racing to demonstrate AI deal momentum and AI-linked revenue growth, but very few have converted that momentum into the kind of locked-in, multi-year recurring contracts that traditional application management and infrastructure outsourcing once provided.

This matters for Indian IT AI monetization more broadly. The sector built its reputation — and its valuation multiples — on annuity-style outsourcing contracts that could be modeled years in advance. AI threatens to disrupt that model in two directions at once: it creates new project-based revenue streams that are harder to forecast, while simultaneously raising questions about whether AI-driven automation will compress the billable-hours model that funded the old annuity business in the first place. Indian IT’s broader ambition of sustaining large-scale growth increasingly hinges on whether firms like TCS can translate today’s AI pilots into tomorrow’s annuity books — a reality check the sector as a whole is only beginning to confront.

Can TCS Build a True AI Annuity Model?

Several levers could eventually convert TCS AI revenue from a project pipeline into a recurring stream:

- Outcome-based managed services: Shifting AI engagements from one-time builds to ongoing “AI operations” contracts, similar to how TCS already manages IT infrastructure on annuity terms.

- Platform monetization: Scaling proprietary platforms such as its cognitive automation platform Ignio into subscription-style, multi-tenant offerings rather than bespoke client builds.

- Autonomous services framework: TCS’s five-level Services Autonomy Framework — modeled on autonomous-vehicle maturity levels — aims to embed AI permanently into delivery, which could eventually justify longer, stickier contracts as clients move from Level 2 to Level 3+ autonomy.

- HyperVault capacity leasing: Converting data-centre infrastructure into long-term hyperscaler and enterprise leases, as described above.

- Mega-deal repetition: TCS has now closed six AI mega deals across five consecutive quarters; converting that cadence into renewal-based relationships rather than one-time wins would meaningfully smooth out TCS AI revenue over time.

None of these are complete yet. That’s precisely why analysts and clients are still describing TCS’s AI business as missing its annuity engine, even as the headline growth numbers impress.

Notably, TCS’s Services Autonomy Framework has already produced measurable results in specific accounts — the company has cited engagements where clients moved from Level 2 to Level 3 autonomy, generating 25–30% productivity gains, and an aerospace client where proactively deployed coding assistants delivered roughly 20% in savings. Results like these are the building blocks of a future annuity model: once a client trusts an autonomous AI operating model enough to run production workloads on it continuously, the natural next step is a long-term managed-services contract rather than a one-time build. The open question is how quickly that trust — and that contract structure — scales across TCS’s enormous delivery organization of nearly 594,000 employees.

What This Means for Enterprise Buyers and Investors

For enterprise technology buyers, the takeaway is practical: TCS AI revenue growth reflects real demand, but engagement structures are still being negotiated deal-by-deal, which means pricing and delivery models remain flexible — and negotiable — for now. For investors, the signal is more cautionary: a $2.6 billion AI run rate sounds impressive against TCS’s roughly $30 billion in FY26 consolidated revenue, but until that AI revenue base stabilizes into recurring contracts, it will continue to show the same lumpiness seen in the swing from $125 million to $75 million in incremental quarterly growth.

The next few quarters — particularly how HyperVault’s hyperscaler negotiations resolve and whether output-based AI pricing models mature into renewal-based contracts — will determine whether TCS AI revenue eventually earns the “annuity” label investors are waiting for.

Frequently Asked Questions

What is TCS’s current AI revenue run rate? TCS AI revenue reached a $2.6 billion annualized run rate in Q1 FY27, up from roughly $2.3 billion in the previous quarter — a 13.6% sequential increase.

What does “annuity engine” mean in the context of TCS’s AI business? An annuity engine refers to a base of long-term, recurring revenue from contracts with predictable renewal cycles, as opposed to project-based revenue that depends on winning and closing individual, time-bound deals each quarter.

Why is TCS’s AI revenue described as “lumpy”? Because incremental quarterly AI revenue fell from about $125 million to about $75 million between Q4 FY26 and Q1 FY27, management itself attributed this volatility to the short-duration, non-recurring, project-based nature of current AI engagements.

Is TCS’s overall business still growing despite the AI annuity gap? Yes. TCS reported total Q1 FY27 revenue of about $7.58 billion, up 13.9% year-on-year, alongside a $9.5 billion order book and its strongest quarterly hiring pace in over three years.

What is HyperVault and how does it relate to TCS’s annuity revenue plans? HyperVault AI Data Center Limited is TCS’s data-centre subsidiary, structured specifically to secure long-term, committed annuity revenue from hyperscalers and AI companies leasing compute capacity — a contrast to the project-based structure of TCS’s client-facing AI services deals.

Could TCS’s AI business eventually become annuity-based? Potentially, through outcome-based managed services, platform monetization (such as Ignio), its Services Autonomy Framework, and HyperVault capacity leasing — but none of these have yet fully matured into a stable, recurring AI revenue base for the company.

How does TCS’s AI growth compare with the rest of the Indian IT sector? Infosys, TCS’s closest large-cap peer, closed FY26 with revenue just above $20 billion and issued cautious FY27 growth guidance of 1.5–3.5% in constant currency, reflecting sector-wide uncertainty about how quickly AI deal pipelines convert into durable, recurring revenue rather than one-time engagements.