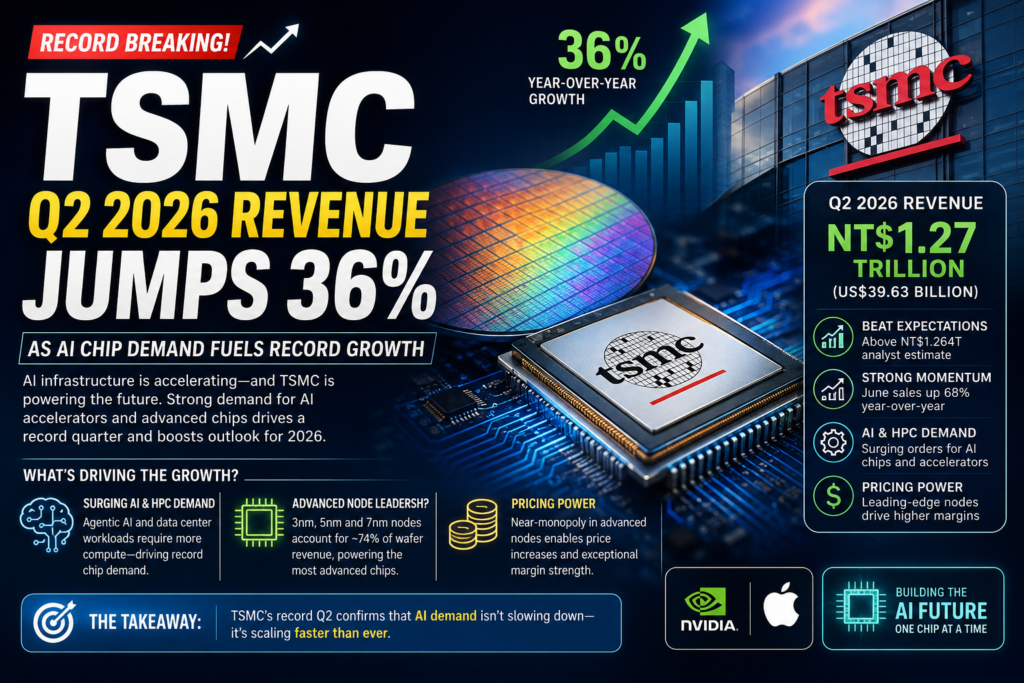

TSMC Q2 2026 revenue hit NT$1.27 trillion (US$39.63 billion), up 36% year-over-year and ahead of analyst forecasts. The world’s largest contract chipmaker delivered this result on the back of surging demand for AI accelerators, HPC processors, and advanced-node manufacturing capacity — confirming that the AI infrastructure buildout is still accelerating rather than slowing down.

For anyone tracking the semiconductor industry, this earnings report is more than just a strong quarter. It’s a real-time gauge of how much AI hardware the world’s biggest tech companies are actually ordering, built, and shipping. Because Taiwan Semiconductor Manufacturing Company sits at the center of the global chip supply chain, its results tend to arrive before the rest of the tech sector reports its own numbers — making this print an early signal worth understanding in detail. Below, we break down the exact figures, the forces driving them, how this quarter compares historically, and what it all means for the rest of 2026.

TSMC Q2 2026 Revenue: The Key Numbers at a Glance

TSMC’s Q2 2026 revenue came in at NT$1.27 trillion, translating to roughly $39.63 billion in U.S. dollar terms. That figure represents a 36% increase compared to the same quarter a year earlier, driven almost entirely by artificial intelligence-related chip orders.

Here’s what stands out about the latest earnings report:

- Beat expectations: An LSEG SmartEstimate compiled from 20 analysts had projected revenue of NT$1.264 trillion — the actual figure came in above that mark.

- Landed near the top of guidance: Management had previously guided second-quarter revenue to fall between $39.0 billion and $40.2 billion, and the result landed comfortably within that range.

- Exceptional June performance: According to Bloomberg’s calculations, sales in June alone rose 68% compared to the same month last year, showing that momentum built sharply as the quarter progressed.

- Concentrated customer base: TSMC remains the primary foundry partner for Nvidia and Apple, two companies at the center of the ongoing AI hardware race.

- Margin strength: Gross margin has remained well above historical averages, supported by pricing increases on the company’s most advanced nodes.

Why This Number Matters Beyond TSMC

Because TSMC manufactures chips for nearly every major AI hardware company on the planet, its quarterly results function as an early indicator for the health of the entire AI supply chain. A strong revenue print from the company suggests that demand for AI GPUs, custom silicon, and high-performance computing hardware isn’t cooling off — it’s still climbing, and it’s climbing faster than many analysts expected even a few months ago.

What Drove TSMC Q2 2026 Revenue Growth?

Direct answer: The primary driver of TSMC Q2 2026 revenue growth was sustained, high-volume demand for AI and high-performance computing chips, combined with the company’s pricing leverage on its most advanced manufacturing nodes.

Three forces combined to push the numbers higher this quarter, and each one is worth unpacking on its own.

Surging AI and HPC Demand

Data center operators, hyperscalers, and AI chip designers continued placing large orders throughout the quarter as the industry shifted from generative AI workloads toward more compute-intensive agentic AI systems. This shift matters because agentic AI — systems capable of planning, reasoning, and executing multi-step tasks with less human oversight — requires significantly more inference and training compute than earlier chatbot-style applications. TSMC executives have described AI-related demand as “extremely robust,” noting that this transition is driving heavier computing requirements across hyperscale data centers rather than representing a simple continuation of prior demand levels.

This isn’t a temporary blip tied to a single product launch. It reflects a structural change in how much silicon is required to run modern AI workloads at scale, and TSMC is the manufacturing bottleneck through which nearly all of that demand must pass.

Advanced Node Technology Leadership

TSMC’s dominance in cutting-edge process nodes remains central to its growth story. In recent reporting periods, 3-nanometer technology accounted for roughly a quarter of wafer revenue, while 5-nanometer and 7-nanometer nodes contributed 36% and 13% respectively. Combined, advanced technologies defined as 7-nanometer and below made up around 74% of total wafer revenue — underscoring how concentrated the company’s growth is in its most sophisticated, and most profitable, manufacturing tiers.

This concentration matters for two reasons. First, it means TSMC’s fortunes are directly tied to whichever chip architectures require the most advanced fabrication — currently, that’s AI accelerators and high-end mobile processors. Second, it gives TSMC substantial negotiating leverage, since very few competitors can match its yields at these node sizes.

Pricing Power on Leading-Edge Nodes

Because TSMC holds a near-monopoly on manufacturing the most advanced chips used in AI accelerators, it has been able to implement price increases on leading-edge nodes without losing customers to competitors. Companies like Nvidia and Apple have limited alternatives if they want access to the smallest, most power-efficient process nodes available today. This pricing power, paired with genuinely high demand, has helped push gross margins well above historical averages, further boosting the dollar-denominated revenue figure this quarter.

TSMC Q2 2026 Revenue vs. Analyst Expectations

Analyst estimates going into the earnings report varied, but nearly all pointed toward strong double-digit growth. Here’s how the actual result compared to the range of expectations circulating before the report:

| Source | Q2 2026 Revenue Estimate | Actual Result |

|---|---|---|

| LSEG SmartEstimate (20 analysts) | NT$1.264 trillion | NT$1.27 trillion |

| TSMC Management Guidance | $39.0B – $40.2B | $39.63B |

| Zacks Consensus Estimate | ~$39.8B (32.2% YoY growth) | $39.63B (36% YoY growth) |

| Bloomberg Analyst Average | ~$39.6B | $39.63B (matched) |

The takeaway: TSMC didn’t just meet guidance, it exceeded the sell-side consensus revenue estimate published by LSEG, and its year-over-year growth rate outpaced several analyst projections that had clustered closer to 32–33% growth. Even Zacks, whose consensus estimate implied slightly higher dollar revenue than the actual result, had projected a lower growth rate — meaning the reported figure told a stronger growth story than the raw dollar comparison alone would suggest.

How This Quarter Stacks Up Against Prior Periods

Looking at recent quarterly performance in context helps clarify whether this growth is a one-time spike or part of a sustained, multi-quarter trend.

| Period | Revenue (USD) | YoY Growth | Key Driver |

|---|---|---|---|

| Q2 2024 | $20.82B | 32.8% | Early AI/HPC ramp |

| Q1 2026 | ~$34.2B (implied) | 35.1% | Leading-edge process demand |

| Q2 2026 Guidance | $39.0B–$40.2B | 29.7%–33.7% | AI accelerator orders |

| Q2 2026 Actual | $39.63B | 36% | AI chip demand, advanced nodes |

Two things jump out from this comparison. First, the company’s year-over-year growth rate has stayed above 30% for multiple consecutive quarters, which suggests this isn’t a one-off surge tied to a single customer or product cycle. Second, the actual Q2 2026 result exceeded the high end of what a simple continuation of Q1 2026’s growth trend would have implied, meaning demand actually accelerated through the quarter rather than merely holding steady.

What This Means for the Broader Semiconductor Industry

A blockbuster earnings report from TSMC doesn’t exist in isolation. Because of the company’s central role in global chip manufacturing, its results ripple across the entire technology sector — from chip designers to cloud infrastructure providers to consumer hardware makers.

Nvidia, Apple, and the AI Hardware Supply Chain

As the primary foundry for both Nvidia and Apple, TSMC’s results offer indirect but meaningful insight into how much AI hardware these companies are actually shipping. Strong revenue growth implies that Nvidia’s AI GPU shipments and Apple’s chip orders remained healthy through the quarter, which should reinforce confidence in the broader AI hardware supply chain heading into those companies’ own upcoming earnings reports. Investors and industry analysts often treat TSMC’s results as a preview of what’s coming from its largest customers roughly two to four weeks later.

Capital Expenditure and Capacity Expansion

TSMC has responded to sustained demand by raising its 2026 capital expenditure outlook toward the high end of a $52–56 billion range — an enormous figure that reflects just how much confidence management has in continued AI-driven demand. Some of the key capacity moves underway include:

- Converting existing 5-nanometer manufacturing tools to support 3-nanometer capacity within Taiwan

- Maintaining flexible capacity across N7, N5, and N3 nodes to serve multiple customer platforms simultaneously

- Progressing development of next-generation A14 process technology, targeted for volume production in 2028, which promises meaningful speed and power efficiency gains over the current N2 node

- Winding down older, less efficient fabs while concentrating investment in high-yield, specialized capacity for mature nodes

This level of capital investment signals that management expects AI-driven demand to persist well beyond a single strong quarter. Building new fab capacity takes years, so a capex increase of this size represents a multi-year bet on continued growth, not a short-term reaction to one good earnings report.

Impact on Smaller Suppliers and the Chip Ecosystem

The effects of this growth extend beyond TSMC’s direct customers. Equipment suppliers, materials providers, and packaging specialists throughout the semiconductor supply chain typically see increased orders when TSMC ramps up capacity. Advanced packaging technologies in particular — used to combine multiple chiplets into a single AI accelerator package — have become an increasingly important bottleneck as demand for AI hardware has grown, and TSMC’s capacity decisions in this area tend to set the pace for the rest of the industry.

TSMC’s Competitive Position in the Global Foundry Market

Understanding why this quarter’s results matter requires some context on where TSMC sits relative to its competitors. The company operates in what’s known as the “pure-play foundry” business — it doesn’t design its own chips, it manufactures chips designed by other companies. This model has made it the default manufacturing partner for nearly every major fabless chip designer in the world.

Market Share and Scale

TSMC holds the majority share of the global pure-play foundry market, and that share climbs even higher when looking specifically at leading-edge nodes below 7-nanometer. Competitors such as Samsung Foundry and Intel Foundry Services have made investments to close the gap, but neither has matched TSMC’s combination of yield rates, capacity, and customer trust at the most advanced process nodes. This scale advantage is part of why the company has been able to raise prices on leading-edge manufacturing without losing significant order volume — customers designing next-generation AI chips have limited alternatives if they want access to the smallest, most efficient nodes currently in mass production.

Why Competitors Struggle to Catch Up

Building a competitive advanced-node foundry isn’t simply a matter of spending money, though the sums involved are enormous. It requires:

- Multi-year lead times to design, construct, and qualify new fabrication facilities

- Deep relationships with equipment suppliers like ASML for extreme ultraviolet (EUV) lithography tools, which are themselves in limited supply

- Accumulated process knowledge and yield optimization built up over successive node generations

- Trust from major customers, who are reluctant to risk product launches on unproven manufacturing partners

This combination of structural advantages helps explain why TSMC has been able to convert surging AI chip demand into outsized revenue growth rather than ceding share to competitors, even as rivals have poured billions into their own advanced-node ambitions.

TSMC’s Outlook for the Rest of 2026

Direct answer: TSMC has reiterated that it expects full-year 2026 revenue to grow by more than 30% in U.S. dollar terms, an upward revision from an earlier forecast of roughly 30%, driven primarily by continued AI and HPC chip demand.

Management has been consistent in messaging that demand for advanced-node capacity remains tight, and that the shift toward agentic AI systems is expected to sustain order volumes through the back half of the year. That said, some analysts have flagged potential gross margin pressure in the second half of 2026, even as top-line growth remains strong, largely due to overseas fab expansion costs and currency fluctuations tied to the U.S. dollar-to-Taiwan dollar exchange rate.

Key Risks to Watch

- Currency exposure: Guidance is based on specific USD/NT dollar exchange rate assumptions; sharp currency swings can meaningfully affect reported dollar-denominated figures even if underlying demand stays constant.

- Geopolitical supply chain risk: As a Taiwan-based manufacturer serving global clients, the company remains sensitive to regional geopolitical developments that could affect production or shipping.

- Margin pressure from overseas expansion: Building capacity outside Taiwan, including new U.S. fabs, typically carries meaningfully higher costs than domestic expansion, which could compress margins even as revenue continues climbing.

- Customer concentration: A significant share of growth is tied to a relatively small number of large customers; any slowdown in AI capital spending from hyperscalers could disproportionately affect results.

Frequently Asked Questions

What was TSMC’s Q2 2026 revenue? Revenue reached NT$1.27 trillion, or approximately $39.63 billion in U.S. dollar terms, for the quarter ended June 30, 2026.

How much did TSMC’s revenue grow year-over-year in Q2 2026? TSMC Q2 2026 revenue grew 36% compared to the same quarter in 2025, exceeding both management guidance and analyst consensus estimates from LSEG and Bloomberg.

What is driving TSMC’s revenue growth in 2026? Growth is primarily driven by AI chip demand, particularly for high-performance computing and AI accelerator chips manufactured on the company’s advanced 3-nanometer and 5-nanometer process nodes.

Did TSMC beat analyst expectations in Q2 2026? Yes. The reported figure came in above the LSEG SmartEstimate of NT$1.264 trillion drawn from 20 analysts, and matched or exceeded several other consensus projections from Zacks and Bloomberg.

What is TSMC’s full-year 2026 revenue forecast? TSMC has guided for full-year 2026 revenue growth of more than 30% in U.S. dollar terms, an upward revision from its earlier 30% forecast, citing sustained AI-related demand across data centers and hyperscale computing.

How does TSMC’s Q2 2026 performance compare to Nvidia and Apple’s outlook? Because TSMC manufactures the majority of Nvidia’s and Apple’s most advanced chips, strong TSMC Q2 2026 revenue growth is generally viewed as a positive early signal for both companies ahead of their own quarterly earnings reports.

Conclusion

TSMC Q2 2026 revenue growth of 36% confirms that AI-driven chip demand remains one of the strongest forces in the global technology economy right now. With advanced nodes accounting for nearly three-quarters of wafer revenue and capital expenditure climbing toward $56 billion to support future capacity, this earnings report is a strong signal — not just for TSMC itself, but for the entire AI hardware ecosystem that depends on its manufacturing capacity. As the industry watches for Nvidia and Apple’s upcoming results, these numbers suggest the AI infrastructure buildout still has considerable room to run through the rest of 2026 and likely well into 2027.