Google Cloud growth reached a historic milestone in Q1 2026, crossing $20 billion in quarterly revenue for the first time — yet the bigger story is what Google couldn’t sell. AI demand is so intense that Alphabet’s CEO confirmed the company left money on the table because it simply didn’t have enough compute capacity to fulfill it. Here’s what happened, why it matters, and what it signals for the future of enterprise AI infrastructure.

What the $20 Billion Milestone Actually Means

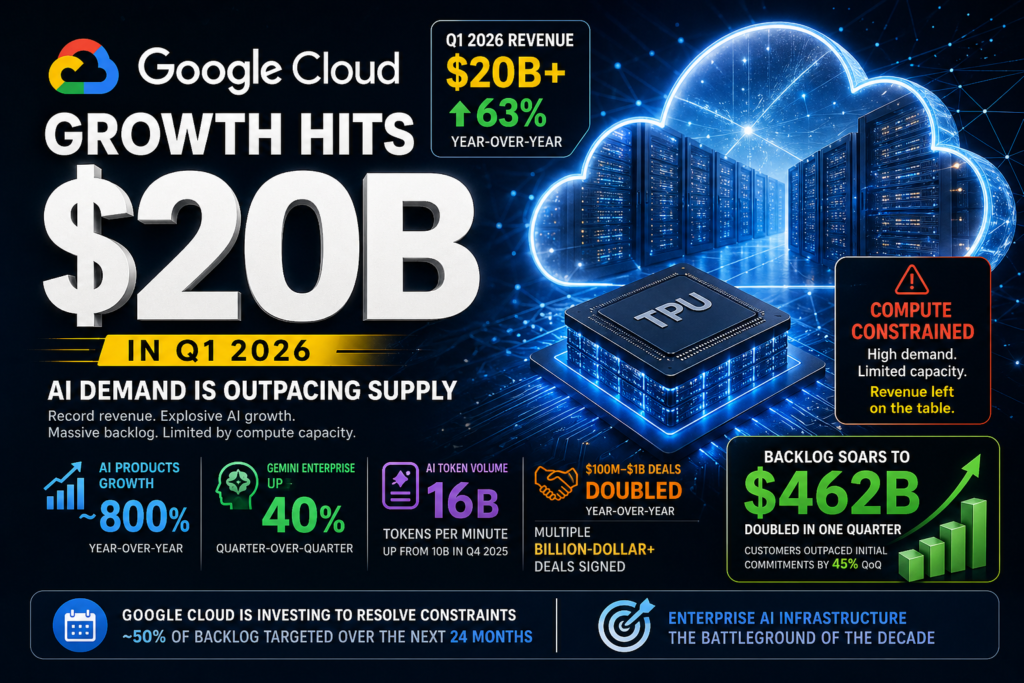

Google Cloud’s Q1 2026 revenue of $20 billion wasn’t just a round number — it represented a 63% year-over-year increase, making it one of the fastest-growing major cloud divisions on the planet. To put that in perspective, the unit had revenues of roughly $12.3 billion in Q1 2025. That’s nearly $8 billion in new quarterly revenue added in a single year.

This isn’t organic business-as-usual growth. It reflects a structural shift: enterprises are no longer experimenting with AI — they’re operationalizing it, and they need cloud infrastructure to do so at scale.

Definition: Google Cloud growth, in this context, refers to the expansion of Alphabet’s cloud computing division, which encompasses Google Cloud Platform (GCP) infrastructure, AI/ML tools, data analytics, and Google Workspace.

The Google Cloud Platform (GCP) segment — the raw infrastructure and AI tooling layer — grew at an even higher rate than the division’s overall 63%. That’s a strong signal that infrastructure spending, not just software subscriptions, is accelerating.

The Engine Behind Google Cloud Growth: Generative AI

Google Cloud growth in Q1 2026 wasn’t driven by legacy workloads migrating to the cloud. It was driven overwhelmingly by generative AI adoption at the enterprise level, with AI solutions identified as the single largest contributor to revenue expansion.

The numbers are striking: products built on Google’s generative AI models grew nearly 800% year-over-year. That’s not a typo. This explosive figure reflects both the low base from a year ago and the genuinely rapid uptake of AI-native applications by enterprises deploying them in production.

Gemini Enterprise Is Pulling Its Weight

Sundar Pichai, Alphabet’s CEO, pointed specifically to Gemini Enterprise as a key growth driver, noting it expanded 40% quarter-over-quarter. That kind of sequential growth — not just year-over-year — indicates sustained momentum, not a one-time spike from early adopters.

Gemini Enterprise is Google’s flagship AI product for business users, enabling organizations to integrate large language models into workflows, documents, meetings, and data analysis. Its acceleration confirms that enterprises are moving beyond pilot projects toward full deployment.

Token Volume as a Growth Signal

One of the most telling metrics Pichai shared: AI token growth via Google’s API reached 16 billion tokens per minute in Q1 2026, up from 10 billion tokens per minute in Q4 2025. That’s a 60% jump in a single quarter, and tokens are the core unit of AI computation — every query, every document processed, every AI interaction consumes them.

More tokens = more AI workloads = more Google Cloud growth. It’s a virtuous cycle as long as capacity can keep up — which, as we’ll see, is the central tension of this earnings report.

The Capacity Constraint Problem Explained

Here’s the uncomfortable truth behind the headline: Google Cloud growth was artificially limited in Q1 2026 because Google didn’t have enough compute infrastructure to meet demand.

Pichai said it plainly on the earnings call: “Our cloud revenue would have been higher if we were able to meet that demand.”

This is unusual language from a tech CEO during an earnings call. Normally, executives are explaining why demand disappointed. Here, Pichai was explaining why supply disappointed — the company had customers ready to spend, and couldn’t fully serve them.

What “Compute Constrained” Really Means for Enterprises

Q: What does it mean for a cloud provider to be “compute constrained”?

A: It means the physical data center capacity — servers, networking, cooling, power, and specialized AI chips (in Google’s case, its proprietary TPUs) — cannot keep pace with the number of customers trying to provision workloads. New customers may face delays in getting capacity, existing customers may hit limits on scaling, and deals that require large reserved capacity can stall.

For enterprises evaluating AI cloud infrastructure, this has real implications:

- Longer provisioning timelines for GPU/TPU-intensive workloads

- Potential deal delays even after contracts are signed

- Premium pricing pressure as scarce capacity commands higher rates

- Risk of capacity lock-in driving customers toward multi-cloud strategies

Pichai acknowledged Google is actively investing to resolve this, describing a “robust, long-range planning framework” focused on data centers and TPU hardware. The company expects to work through roughly 50% of its current backlog over the next 24 months.

Google Cloud vs. Rivals: How Does This Stack Up?

Google Cloud growth at 63% year-over-year is eye-catching, but context matters. Here’s how the major hyperscalers compare on cloud revenue trajectory in early 2026:

| Cloud Provider | Q1 2026 Revenue | YoY Growth | Notable AI Driver |

|---|---|---|---|

| Google Cloud | ~$20.3B | ~63% | Gemini Enterprise, TPU infrastructure |

| Microsoft Azure | Est. ~$43B (segment) | ~33–35% | Azure OpenAI Service, Copilot |

| Amazon AWS | Est. ~$32B | ~17–19% | Bedrock, SageMaker |

Note: Microsoft and Amazon figures are estimates based on analyst consensus for Q1 2026; Google Cloud figure is reported.

The key takeaway: Google Cloud growth rate significantly outpaces its larger rivals, though its absolute revenue base remains smaller. If Google can resolve its capacity bottlenecks, the growth differential could persist — or even widen.

What’s also notable is how Google is competing. Unlike AWS, which dominates through breadth of services, or Azure, which wins through Microsoft enterprise relationships, Google is differentiating on AI-native infrastructure — specifically its custom TPU hardware and the Gemini model family.

The $462 Billion Backlog: Problem or Opportunity?

Perhaps the most jaw-dropping number from Google’s Q1 2026 earnings wasn’t the revenue figure — it was the backlog: $462 billion, which reportedly doubled in a single quarter.

Q: What is a cloud backlog and why does it matter?

A: A cloud backlog represents contracted, committed future revenue — deals that have been signed but not yet fulfilled or recognized as revenue. A backlog doubling in one quarter signals that sales momentum is dramatically accelerating even if current revenue recognition lags behind.

A $462 billion backlog is extraordinary. For context, that figure is larger than the GDP of many mid-sized countries. It represents enterprise customers who have already committed to spending with Google Cloud — they just can’t yet access all the capacity they’ve paid for.

Pichai framed this as a differentiator: the sheer size of the backlog demonstrates long-term confidence in Google Cloud growth from enterprise customers. Deals in the $100 million to $1 billion range doubled year-over-year, and Google signed multiple “billion-dollar-plus” deals in the quarter alone.

Customers also outpaced their initial consumption commitments by 45% quarter-over-quarter — meaning enterprises are using more than they originally contracted for, which is a strong leading indicator of future Google Cloud growth.

What This Means for Businesses Evaluating AI Cloud Infrastructure

If you’re a CTO, IT director, or enterprise technology buyer weighing cloud providers for AI workloads, the Google Cloud Q1 2026 results carry several actionable signals:

Validate capacity availability before committing. The fact that Google itself acknowledged being compute constrained means that procurement timelines for large AI workloads may be longer than expected. Request specific availability windows — not just pricing — during vendor negotiations.

AI-native infrastructure is now a differentiator. Google’s TPU-based infrastructure and Gemini model integration are purpose-built for generative AI. If your workloads are LLM-heavy (fine-tuning, inference at scale, RAG pipelines), Google’s stack deserves serious evaluation against AWS Bedrock and Azure OpenAI Service.

Backlog size signals long-term stability. A $462 billion backlog is a strong indicator that Google Cloud isn’t going anywhere — it reinforces investment confidence for enterprises worried about long-term vendor stability.

Watch the 24-month capacity resolution window. Google says it will work through half the backlog in two years. If capacity constraints ease significantly by mid-2027, enterprises currently facing delays could see substantial improvements in provisioning speed and pricing.

Consider multi-cloud hedging. Capacity constraints at any single provider — including Google — are a genuine operational risk. AI cloud infrastructure strategy should include redundancy planning, particularly for mission-critical inference workloads.

Frequently Asked Questions About Google Cloud Growth in 2026

1. What is driving Google Cloud growth in 2026?

The biggest factor behind Google Cloud growth in 2026 is the explosive rise of artificial intelligence adoption across enterprises. Businesses are no longer simply testing AI tools in small pilot programs. Instead, organizations are deploying AI into real workflows such as customer support automation, software development, analytics, cybersecurity, and document processing.

This shift has created a massive need for cloud infrastructure capable of handling large AI workloads. Google Cloud benefits from this trend because it offers a strong AI ecosystem that combines infrastructure, machine learning services, custom hardware, and enterprise software.

A major contributor to Google Cloud growth is Google’s proprietary TPU (Tensor Processing Unit) infrastructure. Unlike traditional cloud providers that rely heavily on third-party GPUs, Google has built specialized chips optimized for AI training and inference. This gives enterprises more efficient AI processing options and positions Google as a strong player in AI cloud infrastructure.

Another factor accelerating Google Cloud growth is the rapid expansion of Gemini AI services. Enterprises are increasingly adopting Gemini Enterprise for productivity, automation, and workflow integration. As more organizations scale AI across departments, Google Cloud revenue continues to rise.

In short, AI demand is no longer a future trend—it is a present infrastructure requirement, and that is the main reason behind current Google Cloud growth.

2. Why did Google Cloud cross $20 billion in quarterly revenue?

Google Cloud crossed $20 billion in quarterly revenue because enterprise demand for cloud and AI services reached unprecedented levels in Q1 2026.

Historically, Google Cloud was seen as the third major hyperscaler behind AWS and Azure. However, the recent acceleration in AI adoption has reshaped the competitive landscape. Businesses now prioritize providers with strong AI-native infrastructure, which directly benefits Google.

The latest Google Cloud growth milestone reflects multiple revenue streams:

- AI infrastructure consumption

- Data analytics services

- Enterprise productivity tools

- Machine learning APIs

- Generative AI services

The strongest contributor to Google Cloud growth was enterprise AI deployment. Organizations increasingly rely on cloud-based AI models for large-scale operations, which significantly increases compute consumption.

Additionally, more businesses are signing long-term contracts with Google Cloud. These large enterprise commitments contribute to revenue predictability and strengthen future growth potential.

Crossing $20 billion is not just a symbolic number. It signals that Google Cloud growth has entered a new scale category, making it a more serious long-term competitor in cloud computing.

3. What role does AI play in Google Cloud growth?

AI is the central engine behind modern Google Cloud growth.

Before generative AI, cloud adoption was primarily driven by workload migration, storage, and software modernization. While these still matter, AI has introduced an entirely new layer of cloud demand.

AI workloads are resource-intensive. Training large language models, running inference pipelines, managing vector databases, and processing billions of API requests require enormous computational resources.

This creates recurring revenue opportunities for cloud providers.

For Google specifically, AI contributes to Google Cloud growth in several ways:

Infrastructure consumption:

AI workloads consume significant compute resources, increasing spending on TPU and cloud infrastructure.

Model APIs:

Businesses pay for access to Gemini and related APIs.

Enterprise AI tools:

Products like Gemini Enterprise drive SaaS-style recurring revenue.

Data ecosystem integration:

Companies using BigQuery, Vertex AI, and analytics tools often expand cloud commitments.

As AI adoption grows globally, demand for these services increases, further accelerating Google Cloud growth.

Without AI, Google Cloud would still be growing—but likely at a much slower rate.

4. What does “compute constrained” mean for Google Cloud?

When executives say Google is “compute constrained,” they mean customer demand exceeds available infrastructure capacity.

This is one of the most important themes in recent Google Cloud growth discussions.

Cloud providers need physical infrastructure to deliver services, including:

- Data centers

- Servers

- Networking systems

- Cooling systems

- Power supply

- AI accelerators such as TPUs

If too many customers request AI resources simultaneously, providers may run out of deployable capacity.

This means Google had customers ready to spend more money, but infrastructure limitations restricted full revenue capture.

This is unusual because most earnings challenges come from weak demand. In Google’s case, demand is strong—the issue is supply.

For Google Cloud growth, this creates both risk and opportunity.

Risk:

Short-term revenue may be limited.

Opportunity:

Once infrastructure expands, deferred demand can convert into future revenue growth.

This suggests Google Cloud growth could remain strong for multiple quarters if capacity issues are resolved.

5. Is Google Cloud growing faster than AWS and Azure?

In percentage terms, yes—recently Google Cloud growth has outpaced both AWS and Azure.

Google Cloud reported around 63% year-over-year growth, significantly higher than competitors.

This does not mean Google is larger than AWS or Azure.

AWS remains the largest cloud provider globally, followed by Microsoft Azure. Google Cloud is still smaller in absolute revenue.

However, faster Google Cloud growth matters because it indicates momentum.

Why is Google growing faster?

- Strong AI differentiation

- Custom TPU infrastructure

- Gemini ecosystem expansion

- Enterprise AI demand

AWS has scale and breadth, but Google is positioning itself as an AI-first cloud provider.

Azure benefits from Microsoft’s enterprise ecosystem, including Office and Copilot.

Google’s strategy focuses heavily on AI-native workloads, which is currently one of the strongest drivers of Google Cloud growth.

If this trend continues, Google could gradually narrow the competitive gap.

6. What is the significance of Google’s $462 billion backlog?

A backlog represents future contracted revenue that has not yet been recognized.

Google’s reported backlog is highly significant for Google Cloud growth because it indicates strong forward demand.

This means customers have already committed spending to Google Cloud through contracts, reservations, or service agreements.

A large backlog suggests:

- Strong enterprise trust

- Long-term demand visibility

- Revenue pipeline stability

For investors, backlog growth is often viewed positively because it supports future revenue projections.

For customers, it indicates that many organizations are betting on Google as a strategic cloud partner.

The backlog also reinforces that recent Google Cloud growth is not just short-term hype.

Instead, it suggests sustained enterprise adoption and long-term demand for Google Cloud services.

7. How does Gemini Enterprise support Google Cloud growth?

Gemini Enterprise is becoming a major monetization engine for Google Cloud growth.

This platform enables organizations to integrate Google’s AI capabilities into daily business operations.

Common use cases include:

- Content generation

- Workflow automation

- Meeting summarization

- Document analysis

- Coding assistance

- Enterprise search

Because Gemini Enterprise is integrated into Google’s ecosystem, it strengthens product stickiness.

Customers using Gemini often increase dependency on:

- Google Workspace

- Vertex AI

- BigQuery

- Cloud infrastructure

This creates cross-platform revenue expansion.

As adoption rises, Gemini directly and indirectly contributes to Google Cloud growth by increasing both software and infrastructure consumption.

8. Should enterprises choose Google Cloud for AI workloads?

For many AI-heavy organizations, Google deserves serious evaluation.

Google offers several strengths that support Google Cloud growth and make it attractive for enterprises:

AI specialization:

Strong ecosystem around Vertex AI, Gemini, and TPU hardware.

Scalable infrastructure:

Designed for high-performance AI workloads.

Data capabilities:

BigQuery remains a major advantage.

Innovation speed:

Google moves aggressively in AI product development.

However, enterprises should also assess:

- Capacity availability

- Pricing

- Geographic requirements

- Compliance needs

- Vendor lock-in risks

Because Google Cloud growth is happening so rapidly, infrastructure availability may vary depending on region and workload type.

Organizations planning large AI deployments should confirm provisioning timelines early.

9. Will Google Cloud growth continue in 2026 and beyond?

Current indicators suggest yes.

Several factors support continued Google Cloud growth:

- AI adoption remains early

- Enterprise AI budgets are increasing

- Backlog is expanding

- Large contracts are growing

Additionally, Google is investing aggressively in data centers and TPU capacity.

If infrastructure catches up with demand, future quarters could unlock even stronger revenue growth.

However, risks remain:

- Competitive pressure from AWS and Azure

- Regulatory changes

- Capital expenditure intensity

- Execution on capacity expansion

Still, most signals currently support continued Google Cloud growth into late 2026 and beyond.

10. Why should businesses monitor Google Cloud growth?

Businesses should track Google Cloud growth because it reflects broader shifts in enterprise technology.

Rapid cloud growth often signals:

- AI adoption trends

- Infrastructure demand patterns

- Competitive shifts in cloud markets

- Enterprise digital transformation priorities

Monitoring Google Cloud growth helps technology leaders understand where the market is moving.

For investors, it offers insight into Alphabet’s diversification beyond advertising.

For CTOs, it indicates infrastructure trends and vendor competitiveness.

For startups, it highlights where cloud and AI ecosystems are expanding fastest.

In many ways, Google Cloud growth is now a proxy for enterprise AI acceleration itself.

As AI continues reshaping industries, Google Cloud’s trajectory will remain one of the most important indicators in enterprise technology.

Key Takeaways: What to Watch Next

Google Cloud growth crossing $20 billion in a single quarter is a landmark moment — but the underlying narrative is more complex and more interesting than the headline suggests.

Here’s a concise summary of the key facts:

- Revenue: $20B+ in Q1 2026, up 63% year-over-year

- AI products: Grew ~800% YoY; Gemini Enterprise up 40% QoQ

- Token volume: 16 billion tokens/minute, up from 10B in Q4 2025

- Backlog: $462 billion, doubled in one quarter

- Constraint: Compute capacity limited revenue further upside

- Resolution: ~50% of backlog targeted over next 24 months

- Deal size: $100M–$1B deals doubled YoY; multiple billion-dollar-plus signings

For investors, this raises questions about capital expenditure discipline and whether Google can translate backlog into recognized revenue at pace. For enterprises, it’s a signal to engage early with capacity planning. For the broader market, it confirms that AI cloud infrastructure is the defining battleground of the decade — and Google is very much in the fight.

The next key inflection point to watch: Q2 2026 results. If Pichai’s claim that Google Cloud growth was capacity-constrained holds, any meaningful easing of that constraint should produce an outsized revenue acceleration. If growth plateaus, it may suggest demand is softer than the backlog implies.

Either way, Google Cloud has cemented itself as a genuine force in enterprise AI — one that enterprises, investors, and competitors can no longer afford to underestimate.